The Operating Leverage Ratio Imperative for Early Stage Ventures

Professors April Spivack and Michael Morris integrated operating leverage as a component of a firm’s economic input when describing their Entrepreneur’s Profit Model. Operating leverage should be at the forefront of financial and business planning in the early stages of a venture to help direct realistic strategies in the short and long-term. Making the wrong decision about the cost structure to apply in the various stages can threaten the survival of an early-stage venture. In the early stages, staying agile with the ability to adapt quickly suggests a variable cost structure is more beneficial. As the firm scales, investment in infrastructure and employees leads to greater fixed costs but also allows an organization to gain from economies of scale.

This paper will “drill down” on the concept of operating leverage, illustrating its importance. Then, the paper will illustrate the importance of cost structure under various scenarios. Finally, the paper will examine a real-world example where failure to optimize operating leverage led to an organization’s demise.

Introduction

Operating leverage is a measure that assesses the degree to which a company uses fixed costs in its operations. It is a fundamental financial concept with the capability to influence a business's profitability, competitive standing, and strategic direction. It can be defined as the extent to which a firm utilizes fixed costs in its operations. The more a company relies on these costs, the higher its operating leverage.

It's essential to distinguish between operating leverage and financial leverage, as the two serve distinct purposes:

- Operating Leverage: Assesses how changes in sales volume affect a firm's operating income by considering the proportion of fixed and variable costs.

- Financial Leverage: Examines the extent to which debt finances a company's operations, impacting its capital structure and interest obligations.

Operating leverage can be quantified using a common formula that relates the percentage change in operating income (also known as EBIT, Earnings Before Interest and Taxes) to the percentage change in sales. The formula for calculating operating leverage is as follows:

Operating Leverage = (% Change in EBIT) / (% Change in Sales)

In this formula:

- % Change in EBIT represents the percentage change in operating income.

- % Change in Sales represents the percentage change in sales revenue.

Operating leverage essentially measures how sensitive a company's operating income is to changes in sales. A higher operating leverage indicates that a small change in sales can lead to a proportionally larger change in operating income, while a lower operating leverage implies that changes in sales have a less significant impact on operating income.

What comprises a “good” operating leverage differs by industry, age of firm, size of firm, and overall strategy. For startups and early-stage companies, operating leverage tends to be high, especially in the pre-revenue stages since the firm is unable to incur variable expenses like commissions, cost of goods, and royalties until sales occur.

Entrepreneur’s Limited Understanding of Operating Leverage

While it's not accurate to make a broad generalization that entrepreneurs have a difficult time understanding the concept of operating leverage, they may struggle with the concept for various reasons:

- Lack of Financial Background: Many entrepreneurs come from diverse backgrounds, and not all of them have a strong foundation in finance and accounting. Operating leverage involves financial concepts that might be unfamiliar to those without a financial education.

- Focus on Innovation and Product: Entrepreneurs often dedicate significant energy and time to developing innovative products or services, managing day-to-day operations, and growing their businesses. As a result, they might not prioritize learning about complex financial concepts like operating leverage.

- Immediate Concerns: Entrepreneurs often deal with pressing issues related to cash flow, market competition, customer acquisition, and product development. These immediate concerns can sometimes take precedence over learning about financial concepts that might not seem directly relevant now.

- Perceived Complexity: Operating leverage involves understanding the relationship between fixed and variable costs and how changes in sales volume can impact profitability. Developing an understanding of cost behavior (whether costs are fixed or variable in nature) can dramatically improve strategic decision making for areas such as growth opportunities or decline in markets. Being able to make relatively quick cost/benefit decisions is improved as an entrepreneur can quickly evaluate the impact on the bottom line profitability.

- Lack of Exposure: Entrepreneurs who haven't previously worked in a corporate or financial environment might not have been exposed to concepts like operating leverage. Their experiences might be more hands-on and focused on building and managing their businesses.

- Focus on Growth: Entrepreneurs often prioritize growth and expansion. While operating leverage can be important for making informed business decisions, some entrepreneurs might believe that it's not immediately relevant to their growth goals.

Operating Leverage – A Hypothetical Example

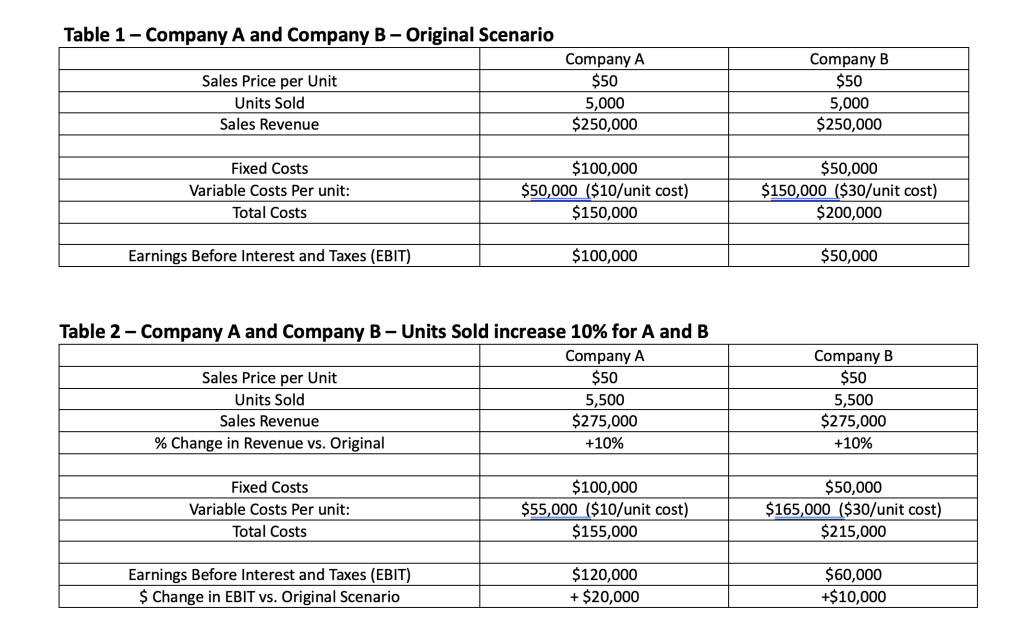

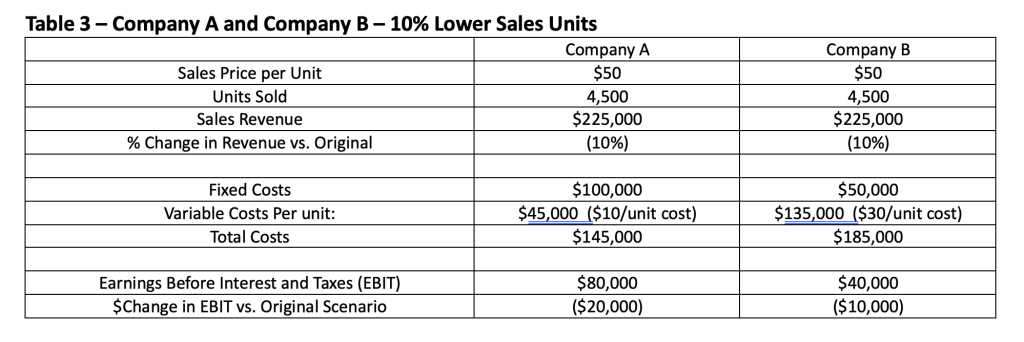

Consider two hypothetical companies: Company A and Company B. Both produce and sell the same product and have the same sales revenue, but they have different cost structures, resulting in different degrees of operating leverage. Then, let's examine that the sales volume for both companies increases by 10% to 5,500 units (in Table 2).

Company A experiences a $20,000 increase in EBIT while Company B sees a $10,000 rise. So, Company A, with a high degree of operating leverage (i.e., higher relative fixed costs) experiences a profitability increase that is double Company B. In an expanding market, having more operating leverage has a great positive impact on profits vs. firms with less operating leverage.

On the other hand, when sales are declining, the weight of more fixed costs has a greater impact on the downside leading to more losses compared to a firm with lower operating leverage. Table 3 shows the effect on bottom-line profits when sales of the two hypothetical firms, A and B, experience a 10% decline in sales units.

Case Study: Operating Leverage in Action

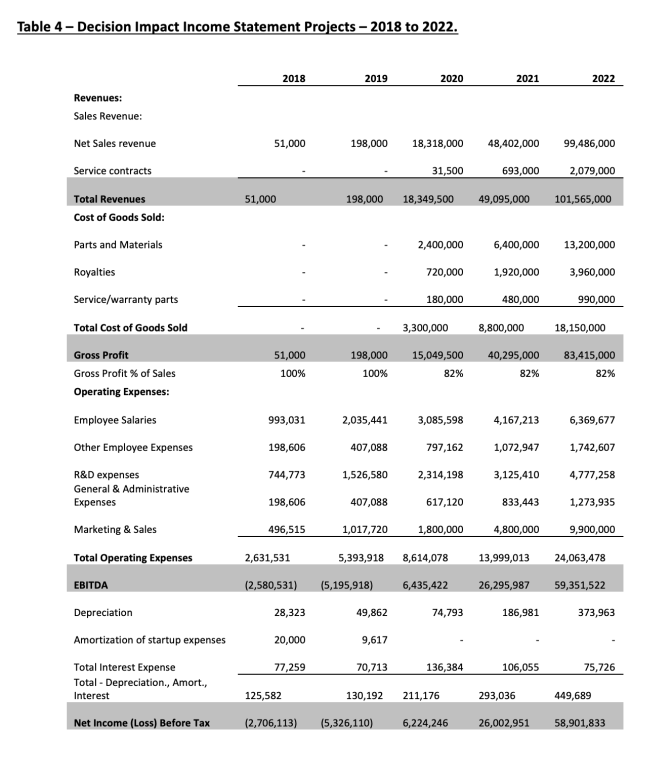

Decision Impact, LLC (name and timing changed to protect confidentiality) was a hot startup that developed a revolutionary tool for the biotech industry that would dramatically speed up organic analysis by up to 100 times faster than their competition at the time. The company was planning to sell its technology at $2M each, had proof of concept, and was receiving significant attention from the VC community. Ultimately, the firm received $15 Million in Round A financing to fund the beta instrument (i.e., customer feedback phase). Previously, the firm existed on bootstrapping and financing from friends and family, with total capital invested prior to the VC round of $2 Million or so over a three-year period. Table 4 is the Income Statement presents Decision Impact’s financial projections for 2018-2022.

Before receiving VC financing, Decision followed a slow, deliberate development process, restricting headcount to two engineers and an office manager resulting in a monthly spend at $50,000. Expenses were routinely examined prior to approval and all deals were constructed on a commission or royalty basis out of future revenues. All team members were involved in making major expenditure decisions.

However, upon receiving their initial VC funding, the cost-conscious mindset changed to a “blitzscaling strategy,” or rapid and aggressive growth. In the context of Decision Impact, blitzscaling involved prioritizing rapid expansion by focusing on increasing user or customer acquisition before the firm had established a solid revenue stream. Expenditures included:

- Hiring a CFO and COO increased monthly burn by $50,000.

- Acquisition of new office and loading space that increased rent by $10,000 per month.

- Once extra space was acquired (4x the previous space) the firm needed to fill it. The hiring of another 10 tech specialists, new desks, and other items – burn increased by $100,000 a month.

- The hiring of expensive law and accounting firms.

- Quarterly Off-Site Retreat meetings for board members and top management.

- Business Class air travel for management.

This occurred just prior to the Covid pandemic. Decision found themselves unable to see customers in their beta testing, causing a substantial delay in tech development. Subsequently, Decision terminated the recently hired technicians and other key personnel in an attempt to conserve cash flow. Yet, despite the terminations, Decision’s operating leverage remained too high in the short run, making it unable to pivot to alternative growth opportunities. As a result, VCs and other shareholders decided it was better to take the firm into bankruptcy instead of continually funding what they believed had become a “zombie company” (i.e., basically a dead company except for minor funding keeping the lights on).

The company lost its mindset about spending as little as needed and became more “fix cost-oriented.” However, when such an event as the pandemic occurred, the company was left with little room to pivot after its spending spree started. Of course, had Covid not occurred, there might have been a different story, but the firm’s high fixed cost structure left little room for maneuvering.

Implications for Startup and Early-Stage Firms

There are a variety of implications for startups and early-stage ventures related to their operating leverage as they often operate in an environment where resources are constrained, and financial stability is crucial. Some of the implications are:

- Risk and Volatility: Startup companies may have a higher degree of operating leverage due to their fixed costs like rent, salaries, and equipment. As shown in the previous example, this means that even small changes in revenue can lead to disproportionately larger changes in profits. While this can amplify gains in good times, it can also magnify losses during periods of low or declining revenue. Therefore, startups with high operating leverage are more exposed to business cycles and market fluctuations.

- Break-Even Point: High operating leverage means that startups have a higher break-even point. In other words, they need to generate a certain level of revenue to cover their fixed costs before they start making a profit. This can put pressure on startups, especially in their early stages, as they strive to achieve profitability.

- Growth and Scale: As a startup grows, it can leverage its fixed costs over a larger revenue base. This can lead to increased profitability as revenue outpaces fixed costs. However, scaling too quickly without a corresponding increase in revenue can strain a startup's financial resources and lead to cash flow issues.

- Flexibility: Startups with high operating leverage may have less flexibility to adapt to changing market conditions. For instance, if there's a sudden drop in demand for their products or services, they might find it challenging to quickly adjust their cost structure due to the fixed nature of their expenses.

- Investor Perception: Investors often assess a startup's financial health based on its ability to manage operating leverage. A startup that can demonstrate a good balance between fixed and variable costs and the ability to weather revenue fluctuations might be seen as a more attractive investment opportunity.

- Financing Challenges: High operating leverage can impact a startup's ability to secure financing. Lenders and investors might be cautious if a startup's cost structure is heavily tilted towards fixed costs, as it increases the risk of default in case of revenue declines.

Guiding Principles for Young Ventures

To mitigate the risks associated with high operating leverage, startup founders should consider these principles:

- Limited Full-Time Employees: Prioritize hiring essential employees, outsourcing other tasks to remain adaptable.

- Variable Payment Structures: Negotiate payment based on revenue percentage with vendors, reducing fixed costs.

- Equity-Based Compensation: Offer stock options or equity-based rewards to employees instead of fixed salaries.

- Smart Asset Purchases: Buy used equipment or negotiate cost-effective solutions to minimize fixed expenses.

Conclusion

Operating leverage wields substantial influence over a startup's trajectory. Founders must navigate this financial concept strategically to strike a balance between fixed and variable costs. By fostering financial resilience, startups can ensure their survival and success in a dynamic market landscape.

Professor Emeritus, Strategy and Entrepreneurship / Management Human Resources / University of Wisconsin - Madison

View Profile