Full Article Abstract

The purpose of this paper is to advance our understanding of an important entrepreneurial behavior—namely habitual entrepreneurship. Employing a cognitive perspective, we examine the association between stable dominant cognitive styles and different behaviors of founding owner-managers. Empirical tests provide support for our premise that a cognitive style is robust in the discrimination between different types of entrepreneurs, and an intuitive style is a significant predictor of habitual entrepreneurship. Our unique two-sample research design both replicates and enhances the validity of our findings. The results of this study have important implications for researchers, practitioners, and investors.

Introduction

Entrepreneurs are a major driving force behind economic development and new job creation. Individuals can become entrepreneurs through two different modes of entry; they can start up new ventures from scratch or they can take over established businesses (Parker & Mirjam van Praag 2012). Although a great deal of research has examined the differences between entrepreneurs and non-entrepreneurs, Sarasvathy (2004) suggests that instead of focusing on these differences, a more fruitful area of research would be to focus on categories among entrepreneurs. In respect to repeat entrepreneurs, researchers (MacMillan, 1986; Westhead and Wright 1998) have differentiated between entrepreneurs with no previous entrepreneurial experience and those who have pursued entrepreneurship prior to their current venture. Novice entrepreneurs are individuals with no prior minority or majority business ownership experience. Habitual entrepreneurs are individuals with prior or concurrent minority or majority business ownership experience. Serial and portfolio entrepreneurs are subsets of habitual entrepreneurs. Serial entrepreneurs have ownership, one at a time, of a series of businesses (Sarasvathy et al. 2013). Portfolio entrepreneurs have simultaneous ownership in two or more businesses (Westhead and Wright 1998; Westhead et al. 2003).

The phenomenon of habitual entrepreneurship has attracted a great deal of scholarly attention and is relevant in the context of both family and non-family owned businesses (Sieger et al., 2011). One reason for this considerable scholarly attention is because habitual entrepreneurs make up a substantial portion of the entrepreneur population (Birley and Westhead, 1993; Carter and Ram, 2003; Ucbasaran et al., 2003; Westhead and Wright, 1998; Westhead et al., 2005a;). It is estimated that one third of owner-managers are habitual entrepreneurs. Westhead and Wright (1998) reviewed studies in the UK indicating that the proportion of habitual entrepreneurs within varied samples ranged from 11.5 to 45.5 percent. More recently, Westhead et al. (2005a) found that among a large sample of business owners, 43.5 percent were habitual (18.6 percent portfolio and 24.9 percent serial). Carter and Ram (2003) reported that portfolio entrepreneurship rates vary by industry, gender, ethnicity, and geographic region with rates of portfolio entrepreneurship in these different segments ranging from 12 percent to 38 percent. In the US, the incidence of habitual entrepreneurship across samples has ranged from 51 percent to as high as 63 percent (Ucbasaran et al., 2003). Despite the variance in reported rates, it is clear that habitual entrepreneurs also make a sizeable contribution to wealth creation in society (Scott and Rosa, 1996) and are an important subset of entrepreneurs.

As stated in entrepreneurship literature, “there is a general consensus that research on novice, serial, and portfolio entrepreneurs is of great interest” (Wiklund and Shepherd, 2008, p. 702). Research has provided a better understanding of the prevalence of entrepreneurship and found some differences between novice and habitual founders based on a handful of individual demographic, background, intentions, and financing variables (e.g., Birley and Westhead 1993; Carter and Ram 2003; Ucbasaran et al., 2009). However, Westhead and Wright (1998) argue that the extant literature has given little attention to the factors and processes underlying habitual entrepreneurship. In response, some researchers have begun to recognize that stable individual differences in cognitions and decision-making may play a crucial role in understanding concurrent and subsequent habitual entrepreneurship behaviors. For example, Ucbasaran et al. (2003) espoused the potential benefits of a cognitive perspective and issued a call for future studies that measure and compare cognitive styles across novice, serial and portfolio entrepreneurs. In another study, Westhead et al. (2005b) found that portfolio entrepreneurs were more creative and innovative than novice entrepreneurs and reported significant differences between these types of entrepreneurs regarding information search and opportunity recognition behaviors. Westhead et al. (2005a, 2005b) concluded that these different types of entrepreneurs likely possess different cognitive mindsets and that future research should examine these differences.

Recent research efforts dealing with habitual entrepreneurs have examined topics such as: the different types of entrepreneurial teams developed by portfolio entrepreneurs (Iacobucci and Rosa, 2010); the prevalence of teams in the firms owned by habitual and first-time entrepreneurs (Tihula and Huovinen, 2010); entrepreneurial learning in the context of portfolio entrepreneurship (Huovinen and Tihula, 2008); the extent and nature of opportunity identification by experienced entrepreneurs (Ucbasaran et al., 2009); passion and habitual entrepreneurship (Thorgen and Wincent, 2013); and habitual entrepreneurs and entrepreneurship addiction (Spivack et al., 2013). Many of these previous studies have focused on different behaviors of habitual entrepreneurs, but not on what fundamentally drives habitual entrepreneurship in the first place. Despite calls for research investigating the cognition of habitual entrepreneurs (e.g., Ucbasaran et al., 2003; Westhead et al., 2005a) few empirical studies have focused on this topic.

The purpose of the current study is to contribute to the entrepreneurship literature by extending our understanding of how stable cognitions of founding owner-managers relate to habitual entrepreneurship. This is an important area of study for many reasons. One reason is because results from this study may shed some light on whether serial and portfolio entrepreneurship is employed solely to increase the wealth of the entrepreneur or, as we propose is employed in part to reduce the stress associated with cognitive misfit and associated coping demands (Kirton 1976, 1989). Having a better understanding of how cognitions relate to habitual entrepreneurship is also important from an investing point of view since angel investors and venture capitalists often base their investment decisions on the entrepreneur and his or her experience as much or more than the type of business the entrepreneur is starting.

Findings from the current study should provide investors with a better understanding of the assets and liabilities of an owner’s stable and preferred cognitive style as it relates to the life-cycle stage of the firm, thus aiding them when making investment decisions. Findings from the current study should also contribute to a better understanding of habitual entrepreneurial behavior and offer insights into the broader entrepreneurial process (MacMillan 1986; Starr and Bygrave 1991), which has implications for practitioners, economic growth and public policy decisions (Westhead et al., 2003).

This paper proceeds as follows: First, we discuss the emerging literature on entrepreneurial cognition and the links to habitual entrepreneurship. Next, we develop and test a series of hypotheses using data on principal founding owner-managers of small to medium enterprises (SMEs) from two distinct sampling frames representing high technology firms and family firms. Finally, we present results and discuss the implications of our findings.

Entrepreneurial Cognition and the Links to Habitual Entrepreneurship

In the extant entrepreneurship literature, entrepreneurs have largely been treated as a homogeneous group. However, a growing literature recognizes that entrepreneurs are in fact heterogeneous with respect to their cognitions (Busenitz and Barney 1997; Mitchell et al., 2002; Mitchell et al., 2007) and differences in cognitive processing lead to different entrepreneurial behaviors and outcomes (Alvarez and Busenitz 2001; Baron 1998, 2004; Katz and Shepherd 2003; Mitchell et al., 2002; Mitchell et al., 2007). Mitchell et al. (2007) argue that entrepreneurial behavior is influenced by cognitions and may not follow the normative/rational model. As described in Mitchell et al. (2002) these cognitions are “knowledge structures used to make assessments, judgments, or decisions involving opportunity evaluation, venture creation, and growth,” and are fundamental to understanding entrepreneurial behavior (p. 97). Over the past decade there has been a growing interest in the application of Cognitive Style Theory in the field of business and management including the area of entrepreneurship (Akinci & Sadler-Smith 2012; Armstrong et al. 2011; Nutt, 2011).

Cognitive Style Theory refers to an individual’s preferred and consistent approach to gathering, processing, and evaluating information (Riding and Rayner 1998; Streufert and Nogami 1989). It affects how people scan the environment for information, interpret this information, and integrate the interpreted information into the theories, models, and schemas that drive their decision-making and behaviors (Hayes and Allinson 1998).

Cognitive style is a broad construct and there are numerous conceptualizations and measures in the literature. The construct can include everything from personality styles (MBTI) to learning styles (Kolb). In this paper we are examining decision-making style which is also classified as a cognitive style. Decision-making styles are conceptualized as highly stable individual preferences in information processing and problem solving. Decision-making styles and are generally set at a young age (Kirton 1976, 1989) and are less likely to change over time than personality or learning styles. In the current study we are looking only at decision styles and a fundamental tenet is that decision styles are stable over time. The stability of decision styles over time is supported by test-retest findings from Allison & Hayes (1996) and also supported by Kirton (1989). Specifically, it has been theorized that decision-making styles are stable (hard-wired) and do not change. More recent research (e.g. Kozhevnikov, 2007) also discusses the validity of the decision style measure and argues that there is stability over time. Thus, we operate on the presumption that cognitive style, as a stable and preferred approach to information processing, will be antecedent to the dependent variables in our study and not likely to be influenced by other factors or change over time. While causality can not be tested in our design, there is strong support that cognitive style is a stable individual characteristic and that it is a key antecedent of specific entrepreneurial behaviors and outcomes.

Models and measure of cognitive style include the Kirton Adaption-Innovation Inventory (KAI) (Kirton 1976) and the Cognitive Style Index (CSI) (Allinson and Hayes 1996). Individual differences in preference for analytical or experiential processing can also be measured using the Rational Experiential Inventory (REI) (Epstein 2010; Akinci and Sadler-Smith 2012). The model and measure of cognitive style used in this study is the Cognitive Style Index (CSI) (Allinson and Hayes 1996). Over the years several studies have either used the CSI or KAI (Allinson and Hayes 1996; Blume and Covin 2011) to measure decision-making style.

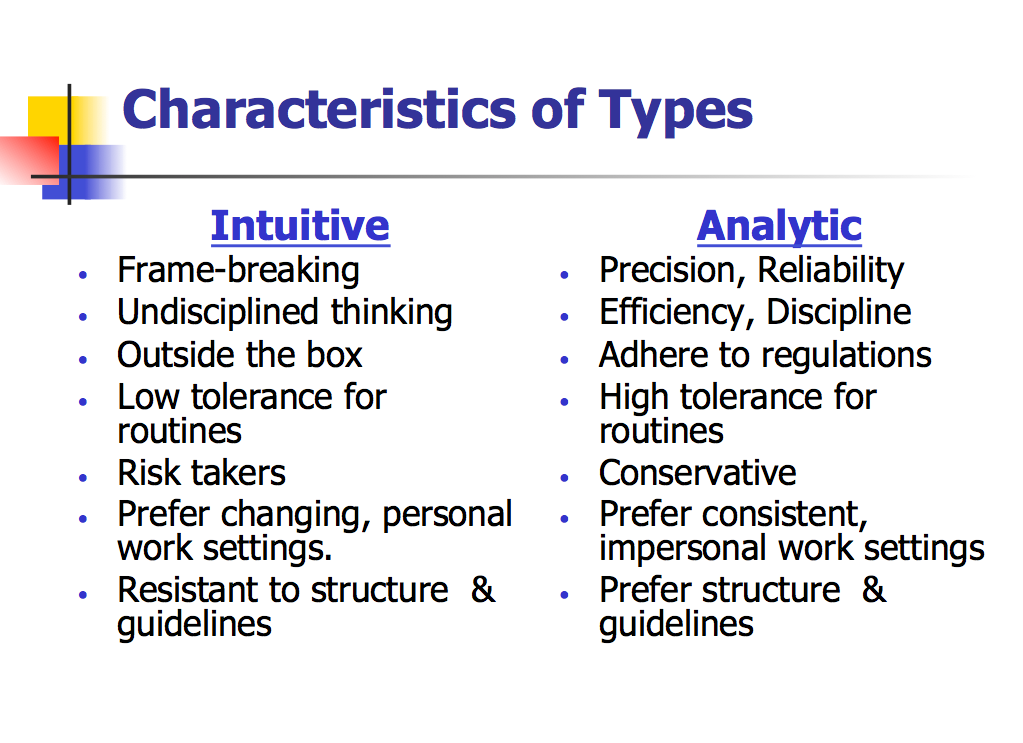

In 1996, Allinson and Hayes presented the initial theoretical development and validation study for the Cognitive Style Index (CSI). The CSI assesses the superordinate intuition-analysis dimension of cognitive style. The CSI measure places individuals on a continuum anchored at one end by a more holistic and heuristic-based logic which is labeled intuitive. Individuals on the intuitive end of the spectrum tend to be relatively nonconformist, prefer an open-ended approach to problem-solving, rely on random methods of exploration and work best with ideas requiring a broad perspective. The other end of the continuum is anchored by more analytic and rational-based logic which is labeled analytic. Analytic individuals favor a more structured approach to problem-solving, prefer systematic methods of investigation and are especially comfortable with ideas requiring sequential analysis (Allinson and Hayes 1996).

Validation studies of the CSI (Allinson & Hayes, 1996) and KAI (Kirton, 1989) both reported very high test – retest stability spanning time periods of up to 17 months (Allison & Hayes, 1996; Kirton, 1989; Kozhevnikov, 2007). For the CSI, test-retest coefficients, which are an indicator of temporal stability have been reported as follows: .82 (Armstrong, Allinson, & Hayes, 1997), .89 (Murphy et al., 1998), and .90 (Allinson & Hayes, 1996). These findings have led Allinson & Hayes (2012, p.11) to conclude that these coefficients, "strongly suggest that scores on the CSI tend to be consistent over time, all other things being equal.”

It is important to note that while an individual’s preferred style will remain constant, when placed in a misfit context (i.e., the situation requires the opposite approach than the individual’s preferred style), Decision-making Style Theory (Allinson & Hayes 1996; Kirton 1976, 1989) proposes that individuals can temporarily employ the non-preferred style – an intuitive person can think analytically and vice versa through the use of coping behavior. However, this approach is not sustainable, and over time the individual in misfit will experience negative psychosocial outcomes (e.g., stress) and be pushed to change the circumstances or their context in order to achieve cognitive fit (Chan 1996; Kirton 1989). Thus, although a person can adopt the other style for brief periods, their preference (preferred style) remains stable.

In situations where individuals have preferences for different work environments based on either a dominant analytic or intuitive orientation, we would expect to find these individuals in occupations that match their dominant style. In a recent review of cognitive styles spanning forty years of management research, Armstrong et al. (2012) concluded that vocational choice was one of the major research areas incorporating cognitive style and that there was a strong relationship among different decision-making styles and professions – including self-employment and entrepreneurship. Research using both the CSI and KAI measures supports this connection (Allinson and Hayes 1996; Sadler-Smith et al. 2000) with individuals in more structured professions having significantly more analytic cognitive styles. Examples of these adaptive/analytic groups include bankers, accountants, and those involved mostly in maintenance or production areas (Chan 1996; Holland 1987; Kirton 1980). Conversely, groups that operate in relatively less structured organizational environments possess styles that are significantly more innovative/intuitive. Examples of these intuitive/innovative groups include marketing, personnel, planning, and research and development (Chan 1996; Holland 1987; Kirton and Pender 1982).

One way that work contexts differ is in terms of the information-processing demands placed on individuals (Hayes and Allinson 1998). On average, the context faced by entrepreneurs tends to be more complex and uncertain than that faced by managers in large organizations (Baron 1998; Blume and Covin 2011; Busenitz & Barney 1997; Covin and Slevin 1991; Hambrick & Crozier 1985; Miller and Friesen 1984). Smith and Miner (1983) proposed that entrepreneurs are more innovative than their managerial counterparts in large US corporations. Buttner and Gryskiewicz (1993) found that entrepreneurs possessed significantly more innovative (using the KAI measure) decision-making styles than managers in large organizations. Allinson et al. (2000) reported that the mean CSI score for Scottish entrepreneurs (high-growth owner-managers) was significantly more intuitive than the mean CSI score from previous samples of managers in general. Most recently Blume and Covin (2011) proposed that “the strength of an entrepreneur’s intuitive cognitive style is positively related to the strength of that entrepreneur’s attributions to intuition as a basis for venture founding decisions.”

Ucbasaran et al. (2003) argued that entrepreneurs can be differentiated based on their greater predilection for heuristic-based thinking and that this can be labeled as entrepreneurial cognition. Ucbasaran et al. (2003) also indicated that the CSI could be a useful measure for differentiating levels of entrepreneurial cognition among novice, serial, and portfolio entrepreneurs. Consistent with Ucbasaran et al. (2003), we theorize that individuals would be more inclined toward novice, serial, or entrepreneurial behavior based on levels of intuitive cognitions. Specific hypotheses are developed below.

Hypothesis Development

Push and Pull Factors

Several researchers have attempted to model and examine the relationship between supply and demand factors that can serve to either “push” and/or “pull” an individual towards exiting a current organization and starting a new venture (Amit and Muller 1996; Schjoedt and Shaver 2007; Shapero and Sokol 1982; Vesper 1983). In particular, Vesper introduces the notion of entrepreneurship “as a path for pursuit of occupational happiness” (1983, p. 40). Vesper defines personal pushes as “negative aspects of present employment which cause individuals to look for something else, either another job or a start-up” (1983, p. 39). For example, unemployment and discontentment with work are possible push variables.

Pull factors can draw an individual toward new venture formation. For example, individuals may be pulled by the lure of independence, the chance to pursue an idea, an attractive market opportunity, offers of financial support and performance rewards (Vesper 1983). These personal pushes and pulls are described as “impelling forces” (Vesper 1983, p. 38), which play an important role in an individual’s decision of whether to leave an organization and start a new venture. We posit that an individual’s cognitive style, both directly and indirectly, by interacting with other relevant variables, can serve to push and/or pull an individual toward entrepreneurship and subsequently influence the likelihood of engaging in habitual entrepreneurial behavior.

Intuitive Cognitive Style as a General Pull Factor toward Entrepreneurship

Allinson and Hayes (1996) theorized that an individual’s preference for work settings is based on the match between an individual’s cognitive style and the information processing demands within work settings. For example, in organizational settings, analytic style individuals would subscribe to the bureaucratic norm and prefer settings that are oriented towards careful routines, governed by logic, and clearly structured and organized. In contrast, intuitive individuals would prefer freedom from rules and regulations and a work setting that is activity-oriented, flexible and unstructured. Allinson et al. (2000) proposed that intuitive approaches to information processing are more compatible with entrepreneurial activity and contexts than rational approaches.

Busenitz and Barney (1997) state that more cautious, methodical and analyzing decision-makers will be attracted to large organizations, while less rational thinkers and those more susceptible to the use of certain biases and heuristics will prefer an entrepreneurial context. Heuristics are simplifying strategies or mental short cuts that individuals may use when making decisions (Tversky and Kahneman 1974), and entrepreneurs are more prone to use heuristics in their decision-making than managers (Baron 1998; Busenitz and Barney 1997; Busenitz and Lau 1996; Forbes 1999). While the use of heuristics is often associated with non-rational processing and sub-optimal outcomes, employing a heuristic-based logic may be more prevalent and advantageous among entrepreneurs who tend to operate in more time sensitive, uncertain and complex contexts (Bird 1988; Busenitz and Barney 1997; Mitchell et al. 2007). Baron (2004) asserts that entrepreneurs possess a more heuristic-based logic and that this plays a role in their decisions to engage in entrepreneurship in the first place.

An intuitive cognitive style, representing a high-order heuristic-based logic, is more compatible with an entrepreneurial context (Brigham and De Castro 2003; Ucbasaran et al. 2003). Individuals vary on the intuitive – analytic dimension, and we theorize that more intuitive owners will experience a stronger pull towards an entrepreneurial context than their more analytic counterparts. Over time, this will be manifested as different ownership patterns. Owners who remain with one firm (novice) will be more analytic than owners who are habitual (serial or portfolio).

Intuitive Cognitive Style and Opportunity Recognition as a Pull Factor

An intuitive cognitive style has been associated with opportunity recognition, which is a key component of entrepreneurship (Shane and Venkataraman 2000). Recent research provides support for developing theoretical links between cognition and opportunity recognition or “entrepreneurial alertness” (Kirzner 1973). Mitchell et al. (2007) state that:

“Developing new ideas and the realization that some people seem particularly alert to new opportunities has had a growing presence in entrepreneurship research in the last decade. Perceiving and interpreting information, and reaching some unique conclusions about entrepreneurial opportunities seem to involve some unique mental processes.” (p.7)

Entrepreneurial alertness has been conceptualized as running on a continuum and that a more heuristic-based cognitive approach may be associated with the more alert end of the continuum (Gaglio and Katz 2001). Thus, more heuristic-based thinking may lead to greater alertness and opportunity recognition and, therefore, it may be a pull factor (Vesper 1983) to pursue entrepreneurial opportunities.

Ucbasaran et al. (2003) presented a series of propositions relating entrepreneurial cognition (high levels of heuristic-based thinking) to alertness and opportunity identification. They propose that, compared to novice entrepreneurs, habitual entrepreneurs (with a more entrepreneurial cognition) will be more alert to entrepreneurial opportunities, and recognize more and better opportunities. Recent empirical evidence supports the specific link between habitual entrepreneurship and opportunity recognition. Westhead et al. (2005a) reported that novice, serial and portfolio entrepreneurs do differ significantly with respect to opportunity identification. They found that novice entrepreneurs identified significantly fewer opportunities than habitual entrepreneurs. Also, portfolio entrepreneurs identified significantly more opportunities than both novice and serial entrepreneurs (Westhead et al. 2005a).

We theorize that an intuitive cognitive style leads to enhanced opportunity recognition, which acts as a pull factor toward entrepreneurial behaviors. Given Westhead et al.’s (2005a) findings, the theoretical implication is that levels of intuitive cognition may be associated with different kinds of entrepreneurial activity and that more intuitive individuals would have greater levels of opportunity recognition and subsequently would be more likely to display habitual behavior. Recent work by Corbett (2005, 2007) provides empirical evidence that there is a significant positive relationship between a more intuitive cognitive style (using the CSI measure) and an increase in opportunities identified.

Cognitive Misfit as a Push Factor

Allinson & Hayes (1996) theorize that an intuitive cognitive style is incongruent with higher levels of firm structure (i.e., in this context we are talking about formal structure where there are formal policies, rules, routines; basically bureaucracy). Whereas formal structure and guidelines are a comfort to the analytic individual, they are viewed as constraining by the intuitive individual. Therefore, higher levels of firm structure produce negative attitudes and intentions to exit the firm for the intuitive entrepreneur (Brigham et al. 2007), possibly serving as a precursor in moving from novice to habitual entrepreneurship. It is important to note however, that while overall complexity might increase when an entrepreneur has a portfolio of businesses, an argument can be made that formal structure/bureaucracy (which is what we are looking at) will not increase at the same rate as complexity. The rationale for this position is that while a business is likely to become more formalized and bureaucratic as it grows and matures, owning another firm simultaneously may offer a portfolio entrepreneur the opportunity to get out of the day-to day operations of the more established firm and divert time and attention back to a more comfortable phase (start-up) in the newer venture. In other words the portfolio entrepreneur will get out of one with more formal structure and get back to a new business with less formal structure. This perspective is consistent with Vesper (1983), who argues that an individual’s negative reactions and discontent with his or her current organizational setting can serve as a strong supply or push factor toward exiting an existing business and subsequent new venture creation.

Brigham et al. (2007) used an owner-manager’s cognitive style (CSI) and the corresponding levels of formal structure in his or her respective firm to operationalize cognitive misfit. They found that in more structured firms, intuitive owner-managers will experience more negative psychosocial outcomes than their more analytic counterparts. Brigham et al. (2007) reported that, while controlling for a number of factors, the interaction of individual style and the levels of structure at the firm level was a significant predictor of the owner-manager’s expressed attitude of dissatisfaction and intentions to exit. Furthermore, dissatisfaction and intentions to exit were shown to be significant predictors of actual exit over a five-year period. Either fully exiting or partially disengaging from a firm to become an owner/manager of another firm concurrently would be a prerequisite for becoming a habitual entrepreneur. Although Brigham et al. (2007) examined the interaction of individual style and the levels of structure at the firm level, their results suggest that there may be a direct link between an intuitive cognitive style, operating through the construct of cognitive misfit, to influence individual attitudes, intentions and actions relevant to habitual entrepreneurial behavior.

We are aware of only three studies that have used holistic/analytic measures of decision-making style in an attempt to differentiate between novice and habitual entrepreneurs. Buttner and Gryskiewicz (1993), using the KAI measure, reported that habitual entrepreneurs were significantly more innovative than novice entrepreneurs. Using a sample of 117 entrepreneurs, Young et al. (2002) reported no significant differences among novice, serial and portfolio entrepreneurs with respect to scores on the CSI. Brigham and De Castro (2003) and Brigham et al. (2007) reported significant correlations between a more intuitive style (CSI) and a greater number of prior businesses owned and/or founded, but did not specifically examine differences among novice, serial and portfolio entrepreneurs.

In spite of these mixed results, it can be reasoned based on the literature reviewed above that an intuitive style is generally more congruent with entrepreneurship than an analytic style. It can also be reasoned that an intuitive cognitive style is linked to enhanced opportunity identification (Corbett, 2007), which pulls an individual to new venture creation. Additionally, it can be reasoned that an intuitive cognitive style interacts with the levels of formal structure of the owner’s firm to potentially create a cognitive misfit situation leading to lower satisfaction, greater intentions to exit and actual exit of the firm (Brigham et al. 2007). This constitutes a strong push force and a necessary condition toward habitual entrepreneurship. It is theorized, then, that an intuitive cognitive style is related to habitual entrepreneurship. Specifically, we theorize that intuitive cognitive style should be a valid predictor of habitual entrepreneurship while controlling for other relevant factors. Thus, we propose the following hypothesis:

H1: A more intuitive cognitive style will be a significant predictor of group membership for habitual entrepreneurs.

We also theorize that different entrepreneurial ownership patterns will be associated with cognitive decision-making styles. Specifically, in order to test the efficacy of cognitive style in discriminating among different types of entrepreneurial behaviors, we put forth the following hypotheses:

H2a: Serial entrepreneurs will possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs.

H2b: Portfolio entrepreneurs will possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs.

Methods

Samples and Research Design

To test our hypotheses, we employ a two-sample design. This allows us to test and replicate our hypothesized relationships across two distinct samples of founding owner-managers of SMEs. Davidsson (2004) espouses the benefits of research designs that allow for within-study replication in entrepreneurship research. Given the mixed findings with respect to CSI differences among novice, serial and portfolio entrepreneurs and the exploratory nature of our inquiry, we believe it is important to replicate the results within the same study. The two samples are described below.

High Technology SMEs

The first sampling frame consisted of an existing database comprised of companies listed in the 2000 Rocky Mountain High Technology Directory. Companies were included if they develop and/or manufacture proprietary products that incorporate state-of-the-art technology or demonstrate significant technical expertise. Subsidiaries and not-for-profit companies were excluded from the sampling frame.

From the total number of 1791 companies listed in the directory, 1294 were retained for inclusion in the study. A total of 267 usable questionnaires distributed in 2001 were returned constituting an effective response rate of 22.1 percent. For the present study, a smaller sub-sample of the original data set was used. This set included only those respondents who were founders of the surveyed firm, were members of the top management team, currently had ownership, were involved in the day-to-day operations of the firm, and whose firms were privately held and had fewer than 250 full-time employees. This left 176 founding owner-managers in the current sub-sample, for which the hypotheses in this study were tested.

Family Firm SMEs

The original completed database consisted of 393 identified family businesses surveyed in 1998 that were identified through both US Chambers of Commerce and student informants. These firms represented a broad spectrum of industries. In 2002, a follow-up study was conducted on these firms completing the original survey. A total of 211 new questionnaires were received, constituting a secondary response rate of 53.6 percent. For this analysis, we only retained firms in which the principal respondent identified the business as a family business, had more than one family member involved in the business, and had more than 15 percent family held ownership. Consistent with the high technology group described above, it was necessary to further refine our sample. Again, the final subset included only those respondents who were founders of the surveyed firm, were members of the top management team, currently had ownership, were involved in the day-to-day operations of the firm, and whose firms were privately held and had fewer han 250 full-time employees. This left 104 founding owner-managers in the current family firm sub-sample for which the hypotheses in this study were tested.

Measures

The following measures were used across both samples. All measures were identical except for owner’s age, which was operationalized differently in the two samples. As is often the case with field survey studies, it is impossible to rule out common method bias. Same-source bias is more common in certain types of questions than others, even within the same self-reported instrument (Crampton and Wagner 1994). Items asking for demographic information seldom exhibit effect-size inflation, and more concrete constructs may be less susceptible than more abstract constructs (Podsakoff and Organ 1986). Many of the items in this study, including the dependent variable, are demographic or factual in nature. Also, great care was taken in the questionnaire to reduce all sources of bias possible through question creation, and ordering. In addition, common method bias is of less concern when we are interested in the individual’s perceptions (e.g., satisfaction, intentions to exit), rather than using self-reports as a proxy for an objective measure (i.e., we are interested in the owner-managers’ perceptions of the demands of their work environments because these perceptions drive their intentions) (Brigham et al., 2007).

Dependent Variable

Type of ownership served as the dependent variable (i.e., Novice, Serial, and Portfolio). Respondents were asked, “How many other businesses have you been involved with, not counting this business, where you were a founder, owner or partner?” Participants were also asked, “Are you currently a founder, owner or partner in another business besides this one?” Based on the responses to these two questions, individuals were classified as either novice, serial, or portfolio entrepreneurs according to the definitions presented earlier in the paper. The habitual category was created by combining serial and portfolio entrepreneurs into a single group, and the variable was dummy coded. It is important to note that novice, serial and portfolio entrepreneurs are potentially nested groups, and it is likely that particular classifications may change over time (i.e., a novice entrepreneur starts another concurrent business). Consistent with other studies on habitual entrepreneurs, the classifications are based on responses for the surveyed firm and thus may be valid only with respect to that point in time (Westhead and Wright 1998).

Independent (Primary Predictor) Variable

Cognitive style served as the independent variable. The CSI (Allinson and Hayes 1996) consists of 38 items and requires the subject to respond to each item on a trichotomous scale (true/uncertain/false); scores on individual items range from 0 to 2, producing a possible total score that ranges from 0 to 76. The closer the total CSI score is to 76, the more analytical the respondent. The closer the CSI score is to 0, the more intuitive the respondent.

To validate the CSI, Allinson and Hayes (1996) administered the CSI to seven different samples totaling almost 1000 subjects. Their findings suggest that the CSI measures a continuous variable that is approximately normal in its distribution and internally consistent with Cronbach’s alpha coefficients ranging from .84 to .92 across the seven sample groups (Allinson and Hayes 1996). Temporal stability was suggested by a test/retest coefficient of .90. Both construct and concurrent validity were demonstrated in the initial validation study (Allinson and Hayes 1996). Sadler-Smith et al. (2000) reported similar reliability coefficients across seven different subject groups totaling over 1000 respondents, and concluded that the CSI displayed both construct and concurrent validity and good reliability across a diverse range of samples. For the high technology sample, α =. 88. For the family firm sample, α =. 87.

Control (Secondary Predictor) Variables

Gender served as one control variable. There are significant differences between men and women with respect to their motivations and choices regarding entrepreneurial activity (Carter et al., 2003). Wiklund and Shepherd (2008) found that men are more likely than women to engage in portfolio entrepreneurship. Respondents were asked to indicate their gender, and the variable was dummy coded.

Owner age served as second control variable. Following previous studies that have examined demographic and human capital variables as predictors of habitual entrepreneurship (e.g., Wiklund and Shepherd 2008), we controlled for owner age. Habitual entrepreneurship might be a function of age in that older individuals simply have more opportunities to become habitual entrepreneurs. Birley and Westhead (1993) reported significant age differences between novice and habitual entrepreneurs. Owner age was ascertained through the respondent indicating one of six categories in the high-technology questionnaire. An owner’s age was simply measured as the respondent’s age in years in the family firm questionnaire.

Satisfaction served as a third control variable. Several researchers have examined the satisfaction of the self-employed (e.g., Katz, 1993) and the role of satisfaction in the nascent entrepreneurial process (Schjoedt and Shaver 2007). Starr and Bygrave (1991) postulated that prior business ownership may provide advantages through experience and learning. Habitual entrepreneurs may possess more realistic expectations of what entrepreneurship entails than their novice counterparts, and this would be reflected in generally higher levels of satisfaction. Satisfaction was measured using a five-item scale developed by Quinn and Staines (1979). They define satisfaction as “affective reaction to the job,” and the definition and measure is intended to refer to and measure what they label as “facet free job satisfaction” (p. 205). This is an established measure of satisfaction and is reviewed in depth by Price and Mueller (1986, pp. 220-223). For the high-technology sample, α = .69. For the family firm sample, α = .71.

Firm performance served as a fourth control variable. Following Wiklund and Shepherd (2008), we used a subjective measure of firm performance. This was measured by a single item where the respondent was asked to rate “the current profit performance of the business relative to the competition” on a seven-point scale ranging from very poor to very good. The underlying premise is that previous ownership experience should translate into greater success of subsequent ventures for habitual owners. Starr and Bygrave (1991) offer a number of possible reasons why prior business ownership might lead to better performance, including acquired skills, networks and expertise.

Intentions to exit served as a fifth control variable. Brigham et al. (2007) found that an owner-managers’ expressed intentions to exit their firms were a significant predictor of an actual exit. Actually exiting an existing firm is a necessary prerequisite for serial entrepreneurship. Also, based on past behavior, habitual entrepreneurs may found new businesses with the strategic intent of leaving their firm earlier in the life-cycle to pursue other opportunities. Intentions to exit were measured using four items, each scored on a 7-point Likert-type scale. These items were employed by O’Reilly, Chatman, and Caldwell (1991), who reported that a Principal Components Analysis yielded a single factor. A sample item asks, “How long do you intend to remain with this organization?” A higher score corresponds to a greater intention to exit. Cable and Judge (1996) reported the internal consistency estimate of this four-item scale as .74. For the high-technology sample, α = .76. For the family firm sample, α = .66.

Analyses and Results

SPSS software was used to conduct the statistical analyses in this study. Following Wiklund and Shepherd (2008), logistic regression was used to test for group membership. ANOVA tests were used to compare group means for the normally distributed continuous CSI.

Descriptive statistics and correlations for all continuous variables for both samples are reported in Table 1. For the set of 176 high-technology founding owner-manager respondents, 75 percent reported that they held at least 50 percent ownership in the firm and the mean number of employees was 26. With respect to gender, 90 percent of the respondents were male. Based on the classification by entrepreneurial ownership type, 69 (39 percent) of the respondents were novice entrepreneurs, and 107 (61 percent) were habitual entrepreneurs. Within the set of habitual entrepreneurs, 49 (28 percent overall; 46 percent of habitual) were serial entrepreneurs, and 58 (31 percent overall; 54 percent of habitual) were portfolio entrepreneurs.

For the set of 104 family firm founding owner-manager respondents, 69 percent reported that they held at least 50 percent ownership in the firm and the mean number of employees was 25. With respect to gender, 73% of the respondents were male. Based on the classification by entrepreneurial ownership type, 43 (41 percent) of the respondents were novice entrepreneurs, and 61 (57 percent) were habitual entrepreneurs. Within the set of habitual entrepreneurs, 32 (31 percent overall; 51 percent of habitual) were serial entrepreneurs, and 29 (28 percent overall; 49 percent of habitual) were portfolio entrepreneurs. The reported rates of novice, serial, portfolio, and habitual entrepreneurship for both samples are consistent with prior research mentioned at the beginning of this paper.

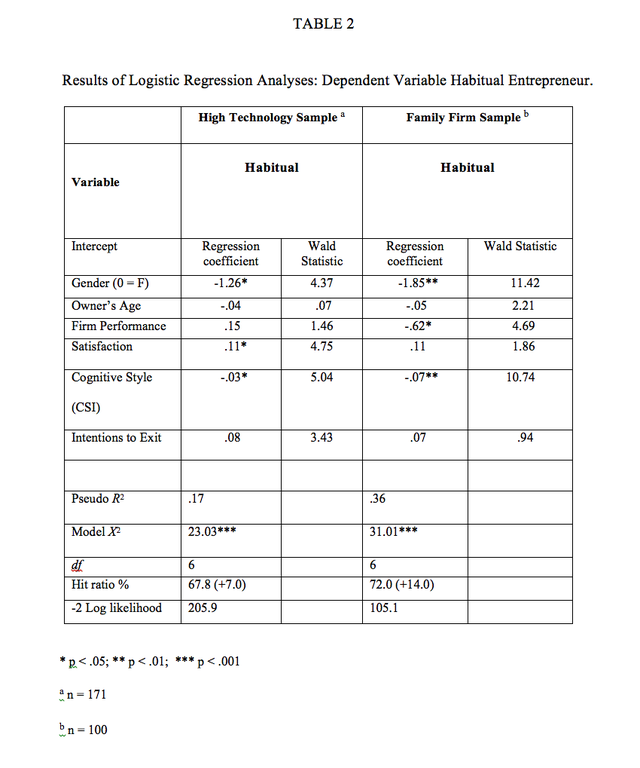

Logistic regression analysis was used to test Hypothesis 1. In the analysis classification as a habitual entrepreneur served as the dependent variable, cognitive style served as the independent variable, and gender, owner’s age, firm performance, satisfaction and intentions to exit served as control variables. This analysis was done for both the family firm sample and the high technology sample.

A total of 171 cases were analyzed (five cases were removed due to missing data on one or more variables) for the high-technology data set and the full model was significantly reliable (chi-square = 23.03, df = 6, p < .001). The model accounted for 17 percent of the variance in habitual entrepreneurship status, with 86.5 percent of habitual entrepreneurs successfully predicted. Overall, 67.8 percent of predictions were accurate. Table 2 provides coefficients and the Wald statistic for each of the independent and control variables. Results indicate possessing a more intuitive cognitive style is significantly associated with being a habitual entrepreneur.

A total of 100 cases were analyzed (four cases were removed due to missing data on one or more variables) for the family firm data set, and the full model was significantly reliable (chi-square = 31.01, df = 6, p < .001). The model accounted for 36 percent of the variance in habitual entrepreneurship status, with 81 percent of habitual entrepreneurs successfully predicted. Overall, 72 percent of predictions were accurate. Table 2 provides coefficients and the Wald statistic for each of the predictor variables. Results indicate that possessing a more intuitive cognitive style is significantly associated with being a habitual entrepreneur. For both the high-technology data set and the family firm data set, Hypothesis 1 which states that a more intuitive cognitive style will be a significant predictor of group membership for habitual entrepreneurs was supported.

Hypotheses 2a and 2b were tested using ANOVA. The results from the ANOVA test for cognitive style scores by novice, serial, and portfolio entrepreneurs are presented in Table 3. A test of homogeneity of variances was not significant, indicating that this assumption was not violated.

The high-technology data set was analyzed first. The overall test (F Statistic) for different mean scores was significant (p = .004). Novice entrepreneurs had a group mean score of 38.4, which is close to the theoretical population mean score (38.5) and past reported scores of general managers (Allinson and Hayes, 1996). Portfolio entrepreneurs were significantly more intuitive than novice entrepreneurs (p < .001) and were the most intuitive group on the CSI measure, with a mean score of 30.5. Results from the analyses do not support H2a, which states that serial entrepreneurs will possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs. However, H2b, which states that portfolio entrepreneurs will possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs, is supported.

The family firm data set was analyzed next. The results of an ANOVA test for cognitive style scores by novice, serial, and portfolio entrepreneurs are presented in Table 3. The overall test (F Statistic) for different mean scores was significant (p = .002). Novice entrepreneurs had a group mean score of 44.7, which is to the analytic side of the theoretical population mean score (38.5) and past reported scores of general managers. Serial entrepreneurs, with a mean score of 34.5, were significantly more intuitive than novice entrepreneurs (p < .001) and were the most intuitive group on the CSI measure. Portfolio entrepreneurs were significantly more intuitive than novice entrepreneurs (p < .05) with a mean score of 37.1. Results from these analyses support H2a, which states that serial entrepreneurs will possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs. Additionally, H2b, which states that portfolio entrepreneurs will possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs is also supported in the family firm sample.

Discussion

In this paper, we extend the recent work on the cognition of entrepreneurs to help explain novice, serial, portfolio and habitual entrepreneurial behavior. Results from the logistical regression analyses show our model was a significant predictor of habitual entrepreneurship status across two distinct samples, and in both samples possessing a more intuitive cognitive style were significant predictors of habitual entrepreneurial behaviors. Furthermore, additional empirical tests demonstrate that within both samples of founding owner-managers, portfolio entrepreneurs were significantly more intuitive on cognitive style than novice entrepreneurs. These results offer general support for our basic premise that cognitive style is an important construct for discriminating between different types of entrepreneurs.

When considering these results it is important to note, however, that the correlation matrix in Table 1 show that the intention to exit in both datasets is significantly negatively correlated to firm performance. Thus, an alternative argument could be made that entrepreneurs simply seem to exit their current business because it does not perform well. This is a very simple and also very likely mechanism. Going into the study, we expected intentions to exit to be negatively correlated with performance and that both variables could be associated with habitual founding behaviors. As such, we controlled for both variables in our regression model. Even while controlling for these important variables, the decision-making style variable was a significant predictor of being a habitual entrepreneur.

A number of factors could influence an owner-manager’s job satisfaction, intentions to exit their firm, and the performance of their firm. We propose that all three of these variables could be important predictors of habitual entrepreneurship behaviors and that they could all be influenced by the owner-manager’s decision-making style. Specifically, research by Brigham et al., (2007) found that both satisfaction and intention to exit were influenced by cognitive style and cognitive misfit and significantly associated with actual turnover (principal no longer with the firm) over a five-year period. Leaving the firm is a prerequisite for serial entrepreneurship. Furthermore, Brigham and Mitchell (2010), again in a study of owner-managers of technology-oriented SMEs, found that cognitive style, level of formalization and their interaction (cognitive fit/misfit) were significantly associated with firm growth over the five-year period. For example, it was shown that the more intuitive the owner-manager’s cognitive style, the higher the growth, while at higher levels of formalization, firms with more intuitive founders had greater growth than firms with more analytic founders. This suggests a link between decision-making style and firm performance.

Based on the research by Brigham et al., (2007), Brigham et al., (2010), and on our findings we believe that cognitive style is an important variable in explaining habitual entrepreneurship, both as a direct predictor and operating indirectly in influencing important factors such as job satisfaction, intentions to exit and firm performance. These factors will also be correlated and likely influence one another. While in this study we have proposed and established an intuitive decision-making style as significantly associated with habitual entrepreneurship, much work is still to be done to understand the specific mechanisms and paths through which decision-making style influences habitual entrepreneurship. However, establishing a significant empirical association among decision-making style and habitual entrepreneurship behaviors is an important first step.

Theoretical Implications

From a theoretical perspective, results from our study suggest that entrepreneurs have different approaches to gathering, filtering and processing information, and making decisions based on that information. These findings have several implications for entrepreneurs, researchers and educators.

First, our results suggest that individuals and current owner-managers possessing a more intuitive cognitive style may be pulled toward entrepreneurial environments that are congruent with their preferred mode of information processing. These results build on prior research that has found intuitive owner-managers (as measured by the CSI) to identify more business opportunities than their more analytic counterparts given similar information (Corbett 2007), which can be a strong pull factor to exit the business (serial) or to remain, but devote resources to concurrently pursue a new opportunity (portfolio).

Second, our results suggest that the more intuitive owner-manager may experience greater cognitive misfit as his or her firm grows and matures. This can lead to negative psychosocial outcomes, which serves as a push force towards habitual entrepreneurship through potential disengagement from his or her firm. This disengagement may be manifested as full divestment, a necessary prerequisite for serial ownership behavior, or as focused attention and effort on another business through concurrent portfolio ownership. These results extend the work of Brigham and De Castro 2003; Brigham et al. 2007), who previously applied cognitive misfit to the study of entrepreneurs.

Third, our results build on work that has examined portfolio entrepreneurship in family firms (e.g., Sieger et al. 2011). Specifically, our results indicate that in family firms, portfolio entrepreneurs possess more intuitive cognitive styles (as measured by the CSI) than novice entrepreneurs. This addresses an important research gap both in the entrepreneurship literature and the family business literature.

Fourth, our results build on the work of DeTienne (2010) which discusses the importance of entrepreneurial exit as a critical component of the entrepreneurial process. Specifically, our results highlight how intuitive cognitive styles can be a factor that leads entrepreneurs to exit the firms they created.

Implications for Practice

Findings from our study also have implications for serial and portfolio entrepreneurs who are affected by the stress associated with cognitive misfit and associated coping demands (Kirton 1976, 1989). Prior research indicates that as organizations age and grow, systems, routines and standardized operating procedures multiply (Blau and Scott 1962; Hanks et al. 1994); structure increases (Dobrev and Barnett 2005); and rational, bureaucratic forms enlarge to conform to institutional norms and rules (Scott, 1975). This pattern of increasing structure often causes transition difficulties (Hambrick and Crozier 1985) and identity conflicts for firm founders (Dobrev and Barnett 2005). The general pattern is an increase in formal structure over time. However, an individual’s cognitive style remains relatively stable over time. For intuitive entrepreneurs, the likely result is a growing cognitive misfit as the firm grows and matures. Habitual entrepreneurs may experience a cognitive misfit (Ucsabaran et al, 2003) and lose interest later in the life cycle when business becomes routine (Wright et al. 1998). Highly intuitive owners may tire of formal structure, bureaucracy and routinization, and this may push them to exit and become habitual entrepreneurs.

Coping behaviors (exhibiting behaviors associated with the non-preferred style) required to handle the conflict between an incongruent preferred style and situational demands (Kirton 1976) are a source of great stress (Pervin 1968). KAI Theory proposes that an individual will change situational circumstances to reduce coping demands or form a team whose combined styles meet situational needs (Kirton 1976; 1989). We posit that serial and portfolio entrepreneurship may, in part, be employed to reduce the stress associated with cognitive misfit and associated coping demands (Kirton 1976, 1989). For example, portfolio entrepreneurs may partially disengage from one firm and focus attention on another new venture, resulting in a horizontal growth strategy (Carter and Ram 2003). Instead of growing their business, the intuitive cognitions of portfolio entrepreneurs may attract them to new ventures. This strategy may be particularly attractive in family firms where fully disengaging from the business carries personal family costs (Sharma et al. 1997).

Implications for Investors

As mentioned earlier, angel investors and venture capitalists often invest based on the entrepreneur as much or more than they invest on the new business in which the entrepreneur is becoming involved. Findings from the current study should provide investors with a better understanding of the assets and liabilities of an owner’s cognitive style as it relates to the life-cycle stage of the firm, thus aiding them when making investment decisions.

Over the years, several studies have attempted to link entrepreneurial experience (habitual ownership) with firm performance. One premise is that for habitual owners' previous ownership experiences should translate into greater success in subsequent ventures. Starr and Bygrave (1991) suggest that the acquired skills, networks and expertise of habitual entrepreneurs should lead to success.

Despite the face validity of this argument, studies have not linked habitual ownership with increased firm performance (Carter and Ram 2003). One explanation for these findings is that prior business ownership could also be a liability. It can be reasoned that a dominant logic (Prahalad and Bettis 1986) developed in a previous successful venture, may not apply in a new context (Baron 2006; Wright et al. 1998). Additionally, managing a business from start-up to maturity is generally problematic for entrepreneurs (Hambrick and Crozier 1985), and it is rare to find entrepreneurs who can do it (Stevenson and Jarillo 1990). One reason for this is that founders often cannot handle managerial routines of mature businesses (Kazanjian 1988; Willard et al., 1992). Thus, over time the value of founders may diminish (Jayaraman et al. 2000), and they may be replaced by professional managers (Boeker and Karichalil 2002; Hanks et al., 1994).

Given that results from our study provide support for the idea that an intuitive style is a significant predictor of habitual entrepreneurship, investors may want to invest in early life cycle firms run by habitual entrepreneurs, but avoid investing in more mature firms run by habitual entrepreneurs. The reason being that a habitual entrepreneur’s intuitive style may be an asset early in a firm’s life cycle when there is incomplete information, time pressure, ambiguity and uncertainty (Allinson et al. 2000); however it may be a liability in a more mature business (Brigham et al. 2007), where founders with more analytic styles may be better suited for the transition to professional management. It is important to note that while an intuitive style may be more common in entrepreneurial samples, it will not always be advantageous. An analytic style is more congruent with planning activities and managing more structured firms. Also, not all entrepreneurial contexts place similar demands on the individual. For example, we could foresee a more analytic style being better suited for buying and running a franchise or an established business.

Limitations and Future Research Directions

As with all studies, our study has limitations associated with it that provide opportunities for future research. In terms of limitations, it should be noted that when identifying differences among novice, serial and portfolio entrepreneurs, researchers are dealing with potentially “nested” groups. Individuals classified as novice entrepreneurs may eventually become serial and/or portfolio entrepreneurs. The classifications in this study were based on ownership history reported at the time of the survey. More complete ownership histories across an entrepreneur’s entire career would offer advantages. The existence of nested groups and the time-dependent nature of classifications could partially explain the wide variations of habitual entrepreneurship reported in different studies. Nesting effects could also limit one’s ability to detect differences among groups, such as the non-significant findings on CSI scores among novice, serial and portfolio entrepreneurs reported by Young et al. (2002). Furthermore, our design did not allow us to examine the ownership and participation levels in businesses other than the one where they were reached for the survey. It seems plausible that differences in cognitive style could be related to different patterns in ownership and management participation.

We also conceptualized habitual entrepreneurship as a distinct outcome that is influenced by the owner-manager’s cognitive style through opportunity recognition. However, it is possible owner experience, as indicated by habitual entrepreneurship, will have a recursive relationship with opportunity recognition. For example, Fiet (2007) presents evidence that successful habitual entrepreneurs will narrow their search to familiar information channels when searching for business opportunities. It may be that their cognitive styles and experience lead habitual entrepreneurs to be alert to opportunities. The interaction of cognitive styles, information search, opportunity recognition, and habitual entrepreneurship deserves more study.

It should also be noted that there may be alternative explanations (factors) regarding the reported relationships in our study. This is also a valid concern, however in Table 2 (Logistic Regression) we do control for several other possible predictors of habitual behavior (e.g., gender, age, firm performance, owner satisfaction, owner intentions to exit). Could there be others? Maybe, however it is not possible to control for everything and we felt these variables made the most sense for which to control. Thus, an area for future research is to examine these and other possible predictors of habitual behavior. For example, gender was a significant predictor of habitual entrepreneurship in our regression model for both samples. Being a female was negatively associated with habitual entrepreneurship. Why women are less likely to be habitual entrepreneurs is an interesting question.

Another opportunity for future research is to employ more sophisticated statistical analyses and longitudinal designs that should allow for the examination of variance accounted for through different pushes and pulls, and the degree to which these may act in combination. If cognitive style influences habitual behavior through a variety of factors, as we have argued, then the aggregate effect of an intuitive cognitive style might be quite large.

Prior research has suggested that the nature of teams may be particularly important in the case of concurrent business ownership (Iacobucci and Rosa 2011; Slevin and Covin 1992). Researchers indicate that portfolio entrepreneurs have more equity partners than novice and serial entrepreneurs, both at founding (Westhead and Wright, 1998) and during ongoing operations (Westhead et al. 2005b; Iacobucci and Rosa 2011). In addition, cognitive diversity among upper-echelon team members can influence firm performance (Miller et al., 1998). Thus, another area of future research would be to examine how the cognitive makeup of team members may influence novice and portfolio ownership patterns.

In addition to providing a foundation for the future research efforts discussed above, our findings also provide a foundation for future research efforts that examine why entrepreneurs may delay business failure even when doing so may be financially costly to them (see Shepherd et al. 2009 for a discussion of the financial and emotional costs associated with business failure). Specifically, it would be interesting to examine if novice, serial or portfolio entrepreneurs are more prone to delay business failure and if the distinctive cognitive styles associated with each group drive of this type of decision-making. Additionally, building on the work of Kickul et al., (2009) another interesting research question to examine is whether people with a strong intuitive orientation are good in perceiving business opportunities (exploration) but not good in running a firm (exploitation).

Conclusions

Macmillan (1986) stated that to really understand entrepreneurship, we should study habitual entrepreneurs. More recently, there have been several calls for studies comparing habitual entrepreneurs using cognitive measures and, specifically, measures of cognitive style (Ucbasaran et al. 2003; Westhead et al. 2005b). In this study, we provide evidence that novice, serial and portfolio entrepreneurs do possess distinctive cognitive styles. Furthermore, the regression analyses performed on two samples support our premise that an intuitive cognitive style is significantly associated with habitual entrepreneurship. Our innovative two-sample design allowed us to replicate this finding, adding to the strength of our contribution. Thus, our results support the importance and utility of using a cognitive perspective to better understand habitual entrepreneurial behaviors.

References

Akinci C., Sadler-Smith, E. (2012). Intuition in management research: A historical review. International Journal of Management Reviews, 14, 104-122. Allinson, C.W., Chell, E., Hayes, J., (2000). Intuition and entrepreneurial performance. European Journal of Work and Organizational Psychology, 9, 31-43.

Allinson, C.W., Hayes, J., (1996). The cognitive style index: a measure of intuition-analysis for organizational research. Journal of Management Studies, 33, 119-135.

Alvarez, S.A., Busenitz, L.W., (2001). The entrepreneurship of resource based theory. Journal of Management, 27, 755-775.

Amit, R., Muller, E., (1996). “Push” and “pull” entrepreneurship. Small Business and Entrepreneurship, 12, 64-80.

Armstrong, S., Cools, E., Sadler-Smith, E., (2011). Role of cognitive styles in business and management: Reviewing 40 years of research. International Journal of Management Reviews, published online.

Baron, R.A., (1998). Cognitive mechanisms in entrepreneurship: why and when entrepreneurs think differently than other people. Journal of Business Venturing, 13, 275-294.

Baron, R.A., (2004). The cognitive perspective: a valuable tool for answering entrepreneurship’s basic “why” questions. Journal of Business Venturing, 19, 221-239.

Baron, R.A., (2006). Opportunity recognition as pattern recognition: How entrepreneurs “connect the dots” to identify new business opportunities. Academy of Management Perspectives, 20, 104-119.

Bird, B.J., (1988). Implementing entrepreneurial ideas: The case for intention. Academy of Management Review, 13, 442-453.

Birley, S., Westhead, P., (1993). A comparison of new businesses established by “novice” and “habitual” founders in Great Britain. International Small Business Journal, 11, 535-557.

Blau, P.M., Scott, W.R., (1962). The Structure of Organizations. New York: Basic Books.

Blume, B., Covin, J., (2011). Attributions to intuition in the venture founding process: Do entrepreneurs actually use intuition or just say they do? Journal of Business Venturing, 26, 137-151.

Boeker, W., Karichalil, R., (2002). Entrepreneurial transitions: factors influencing founder departure. Academy of Management Journal, 45, 818-826.

Brigham, K.H., De Castro, J.O., (2003). Entrepreneurial fit: the role of cognitive misfit, in: Katz J.A., Shepherd D.A. (Eds.), Advances in Entrepreneurship, Firm Emergence, and Growth. Elsevier/JAI Press, Oxford, UK, pp. 37-72.

Brigham, K.H., De Castro, J.O., Shepherd, D.A., (2007). A person-organization fit model of owner-managers’ cognitive style and organizational demands. Entrepreneurship Theory & Practice, 31, 29-51.

Brigham, K.H., Mitchell, R.K., and De Castro, J.O. (2010). Cognitive misfit and firm growth in technology-oriented SMEs. International Journal of Technology Management, 52, 4-25).

Busenitz, L.W., Barney, J.B., (1997). Differences between entrepreneurs and managers in large organizations: Biases and heuristics in strategic decision-making. Journal of Business Venturing, 12, 9-30.

Busenitz, L.W., Lau, C., 1996. A cross-cultural cognitive model of new venture creation. Entrepreneurship Theory & Practice, 20, 25-39.

Buttner, H.E., Gryskiewicz, N., (1993). Entrepreneurs’ problem-solving styles: an empirical study using the Kirton adaptation/innovation theory. Journal of Small Business Management, 31, 22-31.

Cable, D.M., Judge, T.A., (1996). Person-organization fit, job choice decisions, and organizational entry. Organizational Behavior & Human Decision Processes, 67(3), 294-311.

Carter, N.M., Gartner, W.B., Shaver, K.G., Gatewood, E.J., (2003). The career reasons of nascent entrepreneurs. Journal of Business Venturing, 18(1), 13-39.

Carter, S., Ram, M., (2003). Reassessing portfolio entrepreneurship: towards a multidisciplinary approach. Small Business Economics, 21, 371-380.

Chan, D., (1996). Cognitive misfit of problem solving style at work: a facet of person-organization fit. Organizational Behavior and Human Decision Processes, 68, 194-207.

Collewaert, V., (2012). Angel investors‘ and entrepreneurs‘ intentions to exit their ventures: A conflict perspective. Entrepreneurship Theory & Practice, 36(4), 753- 779.

Corbett, A.C., (2005). Experiential learning within the process of opportunity identification and exploitation. Entrepreneurship Theory & Practice, 29, 473-491.

Corbett, A.C., (2007). Learning asymmetries and the discovery of entrepreneurial opportunities. Journal of Business Venturing, 22(1), 97-118.

Covin, J.G., Slevin, D.P., (1991). A conceptual model of entrepreneurship as firm behavior. Entrepreneurship Theory & Practice, 16, 7-25.

Crampton, S.M., Wagner, J.A., (1994). Percept inflationin micro-organizational research: an investigation of prevalence and effect. Journal of Applied Psychology, 79(1), 67-76.

Davidsson, P., (2004). Researching Entrepreneurship. New York: Springer.

DeTienne, D., (2010). Entrepreneurial exit as a critical component of the entrepreneurial process: Theoretical development. Journal of Business Venturing, 25(2), 203-215.

Dobrev, S.D., Barnett, W.P., (2005). Organizational roles and transition to entrepreneurship. Academy of Management Journal, 48, 433-449.

Epstein, S. (2010). Demystifying intuition: What it is, what it does, and how it does it. Psychological Inquiry, 21(4), 295-312.

Fiet, J.O., (2007). A prescriptive analysis of search and discovery. Journal of Management Studies, 44(4), 592-611.

Forbes, D.P., (1999). Cognitive approaches to new venture creation. International Journal of Management Reviews, 1, 415-439.

Gaglio, C.M., Katz, J.A., (2001). The psychological basis of opportunity identification: entrepreneurial alertness. Small Business Economics, 16, 95-111.

Hambrick, D.C., Crozier, L., (1985). Stumblers and stars in the management of rapid growth. Journal of Business Venturing, 1, 31-45.

Hanks, S.H., Watson, C.J., Jansen, E., Chandler, G.N., (1994). Tightening the life-cycle construct: a taxonomic study of growth stage configurations in high-technology organizations. Entrepreneurship Theory & Practice,18 (2), 5-27.

Hayes, J., Allinson, C.W., (1998). Cognitive style and the theory and practice of individual and collective learning in organizations. Human Relations, 51, 847-871.

Holland, P.A., (1987). Adaptors and innovators: application of the Kirton adaption-innovation theory to bank employees. Psychological Reports, 60, 339-342.

Huovinen, J., Tihula, S. (2008). Entreprenurial learning in the context of portfolio entrepreneurship. International Journal of Entrepreneurial Behaviour & Research, 14(3), 152-171.

Iacobucci, D., Rosa, P., (2010). The growth of business groups by habitual entrepreneurs: The role of entrepreneurial teams. Entrepreneurship Theory and Practice, 34(2), 351-377.

Jayaraman, N., Khorana, A., Nelling, E., Covin, J., (2000). CEO founder status and firm financial performance. Strategic Management Journal, 21, 1215-1224.

Katz, J.A. (1993). How satisfied are the self-employed: A secondary analysis approach. Entrepreneurship Theory and Practice, 17, 35-51.

Katz, J.A., Shepherd, D.A., (2003). Cognitive approaches to entrepreneurship research, in Katz J.A., Shepherd, D.A. (Eds.), Advances in Entrepreneurship, Firm Emergence, and Growth. Elsevier/JAI Press, Oxford, UK, pp. 1-11.

Kazanjian, R.K., (1988). Relation of dominant problems to stages of growth in technology-based new ventures. Academy of Management Journal, 31: 257-279.

Kickul, J., Gundry, L. K., Barbosa, S. D., & Whitcanack, L. (2009). Intuition versus analysis? Testing differential models of cognitive style on entrepreneurial self-efficacy and the new venture creation process. Entrepreneurship Theory and Practice, 33: 439–453.

Kirton, M.J., (1976). Adaptors and innovators: a description and measure. Journal of Applied Psychology, 61, 622-629.

Kirton, M.J., (1980). Adaptors and innovators in organizations. Human Relations, 3, 213-224.

Kirton, M.J., (1989). Adaptors and Innovators, Routledge, London.

Kirton, M.J. Pender, S.R., (1982). The adaption-innovation continuum: Occupational type and course selection. Psychological Reports, 51, 883-886.

Kirzner, I.M., (1973). Competition & Entrepreneurship, University of Chicago Press, Chicago,

Kozhevnikov, M., (2007). Cognitive styles in the context of modern psychology: Toward an integrated framework of cognitive style. Psychological Bulletin, 133(3), 464-481.

MacMillan, I.C., (1986). To really learn about entrepreneurship, let’s study habitual entrepreneurs. Journal of Business Venturing, 1, 241-243.

Miller, C.C., Burke, L.M., Glick. W.H., (1998). Cognitive diversity among upper echelon executives: Implications for strategic decision processes. Strategic Management Journal, 19, 39-58.

Miller, D., Friesen, P.H., 1984. Organizations: A Quantum View, Prentice Hall, Englewood Cliffs, NJ.

Mitchell, R.K., Busenitz, L.W., Bird, B., Gaglio, C.M., McMullen, J.S., Morse, E.A., & Smith, J.B., (2007). The central question in entrepreneurial cognition research 2007. Entrepreneurship Theory & Practice, 31, 1-27.

Mitchell, R K., Busenitz, L.W., Lant, T., McDougall, P.P., (2002). Toward a theory of entrepreneurial cognition: rethinking the people side of entrepreneurship research. Entrepreneurship, Theory, & Practice, 27, 93-105.

Murphy, H. J., Kelleher, W. E., Doucette, P. A. & Young, J. D. (1998). Test-retest reliability and construct validity of the Cognitive Style Index for business undergraduates.

Psychological Reports, 82, 595-600.

Nutt, P., (2011). Making decision-making research matter: Some issues and remedies. Management Research Review, 34(1), 5-16.

O’Reilly, C.A.III, Chatman, J., Caldwell, D.F., 1991. People and organizational culture: A profile comparison approach to assessing person-organization fit. Academy of Management Journal, 34: 487-516.

Parker, S, Mirjam van Praag, C., (2012). The entrepreneur’s mode of entry: Business takeover or new venture start? Journal of Business Venturing, 27, 31-46.

Pervin, L.A., 1968. Performance and satisfaction as a function of individual-environment fit. Psychology Bulletin, 69, 56-68.

Podsakoff, P.M., Organ, D.W., (1986). Self-reports in organizational research: problems and prospects. Journal of Management, 12(4), 531-543.

Prahalad, C.K., Bettis, R.A., 1986. The dominant logic: A new linkage between diversity and performance. Strategic Management Journal, 7, 485-501.

Price, J.L. & Mueller, C.W., 1986. Handbook of organizational measurement, Ballinger, Cambridge, MA.

Quinn, R.P., Staines, G.L., (1979). The 1977 quality of employment survey, University of Michigan Press, Ann Arbor, MI.

Riding, R. J., Rayner, S.G., (1998). Cognitive Styles and Learning Strategies, Fulton, London.

Rocky Mountain High Technology Directory, 2000. Leading Edge, Ashland, OR.

Sadler-Smith, E., Spicer, D.P., Tsang, F., (2000). Validity of the cognitive style index: replication and extension. British Journal of Management, 11, 175-181.

Sarasvathy, S., (2004). The questions we ask and the questions we care about: Reformulating some problems in entrepreneurship research. Journal of Business Venturing, 19(5), 707-717.

Sarasvathy, S., Menon, A., Kuechle, G., (2013). Failing firms and successful entrepreneurs: serial entrepreneurship as a temporal portfolio. Small Business Economics, 40(2), 417-434.

Schjoedt, L. & Shaver, K.G., (2007). Deciding on an entrepreneurial career: A test of the pull and push hypotheses using the panel study of entrepreneurial dynamics data. Entrepreneurship Theory & Practice, 31(5), 733-752.

Scott, W.R., (1975). Organization structure, in: Inkeles, A. (Ed.), Annual Review of Psychology. Annual Reviews, Palo Alto, CA, pp. 1-20.

Scott, M. & Rosa, P., (1996). Has firm level analysis reached its limits? International Small Business Journal, 14, 81-99.

Shane, S.A.,Venkataraman, S., (2000). The promise of entrepreneurship as a field of research. Academy of Management Review, 25(1), 217-226.

Shapero, A., Sokol, L., (1982). The social dimensions of entrepreneurship, in: Kent, C.A., Sexton, D.L., Vesper, K.H. (Eds.), Encyclopedia of Entrepreneurship, Prentice Hall, Englewood Cliffs, NJ, pp.72-90.

Sharma, P, Chrisman, J.J., Chua, J. H., (1997). Strategic management of the family business: Past research and future challenges. Family Business Review, 10, 1, 1-35.

Shepherd, D., Wiklund, J., Haynie, J., (2009). Moving forward: Balancing the financial and emotional costs of business failure. Journal of Business Venturing, 24, 134 – 148.

Sieger, P., Zellweger, T., Nason, R., Clinton, E., (2011). Portfolio entrepreneurship in family firms: A resource-based perspective. Strategic Entrepreneurship Journal, 5, 327-351.

Slevin, D.P., Covin, J.G., (1992). Creating and maintaining high-performance teams, in:

Sexton, D.L., Kasarda, K.D. (Eds.), The State of the Art of Entrepreneurship. PWS-Kent Publishing Company, Boston, MA, pp. 358-386.

Smith, N.R., Miner, J.B., (1983). Type of entrepreneur, type of firm, and managerial motivation: implications for organizational life cycle theory. Strategic Management

Journal, 4, 325-340.

Spivack, A., McKelvie, Haynie, J. (2013). Habitual entrepreneurs: Possible cases of entrepreneurship addiction. Journal of Business Venturing, December: Online.

Starr, J., Bygrave, W., (1991). The assets and liabilities of prior start-up experience: an exploratory study of multiple venture entrepreneurs, in Churchill, N.C., Bygrave, W.D., Covin, J.G., Sexton, D.L., Slevin, D.P., Vesper, K.H., Wetzel, W.E.,(Eds.), Frontiers of Entrepreneurship Research, Babson College, Wellesley, MA, pp. 213-227.

Stevenson, H., Jarillo, J., (1990). A paradigm of entrepreneurship: entrepreneurial management. Strategic Management Journal, 11, 17-27.

Streufert, S., Nogami, G. Y., (1989). Cognitive style and complexity: implications for I/O psychology, in Cooper, C.L., Robertson, I. (Eds.), International Review of Industrial and Organisational Psychology, Wiley, Chichester, pp. 93-143.

Tihula, S., Huovinen, J. (2010). Incidence of teams in the firms owned by serial, portfolio and first-time entrepreneurs. International Entrepreneurship and Management Journal, 6, 249-260.

Thorgren, S. & Wincent, J. (2013). Passion and habitual entrepreneurship. International Small Business Journal, June: Online.

Tversky, A., Kahneman, D., (1974). Judgment under uncertainty: heuristics and biases. Science, 185, 1124-1131.

Ucbasaran, D., Wright, M., Westhead, P., Busenitz, L. W., (2003). The impact of entrepreneurial experience on opportunity identification and exploitation: habitual and novice entrepreneurs, in Katz J.A., Shepherd, D.A. (Eds.), Advances in Entrepreneurship, Firm Emergence, and Growth. Elsevier/JAI Press, Oxford, UK, pp. 231-264.

Ucbasaran, D., Westhead, P., Wright, M. (2009). The extent and nature of opportunity identification by experienced entrepreneurs. Journal of Business Venturing, 24(2), 99-115.

Vesper, K. H. (1983). Entrepreneurship and National Policy. Chicago, IL: Walter E. Heller

Westhead, P., Ucbasaran, D., Wright, M., (2003). Differences between private firms owned by novice, serial, and portfolio entrepreneurs: Implications for policy-makers and practitioners. Regional Studies, 37, 187-200.